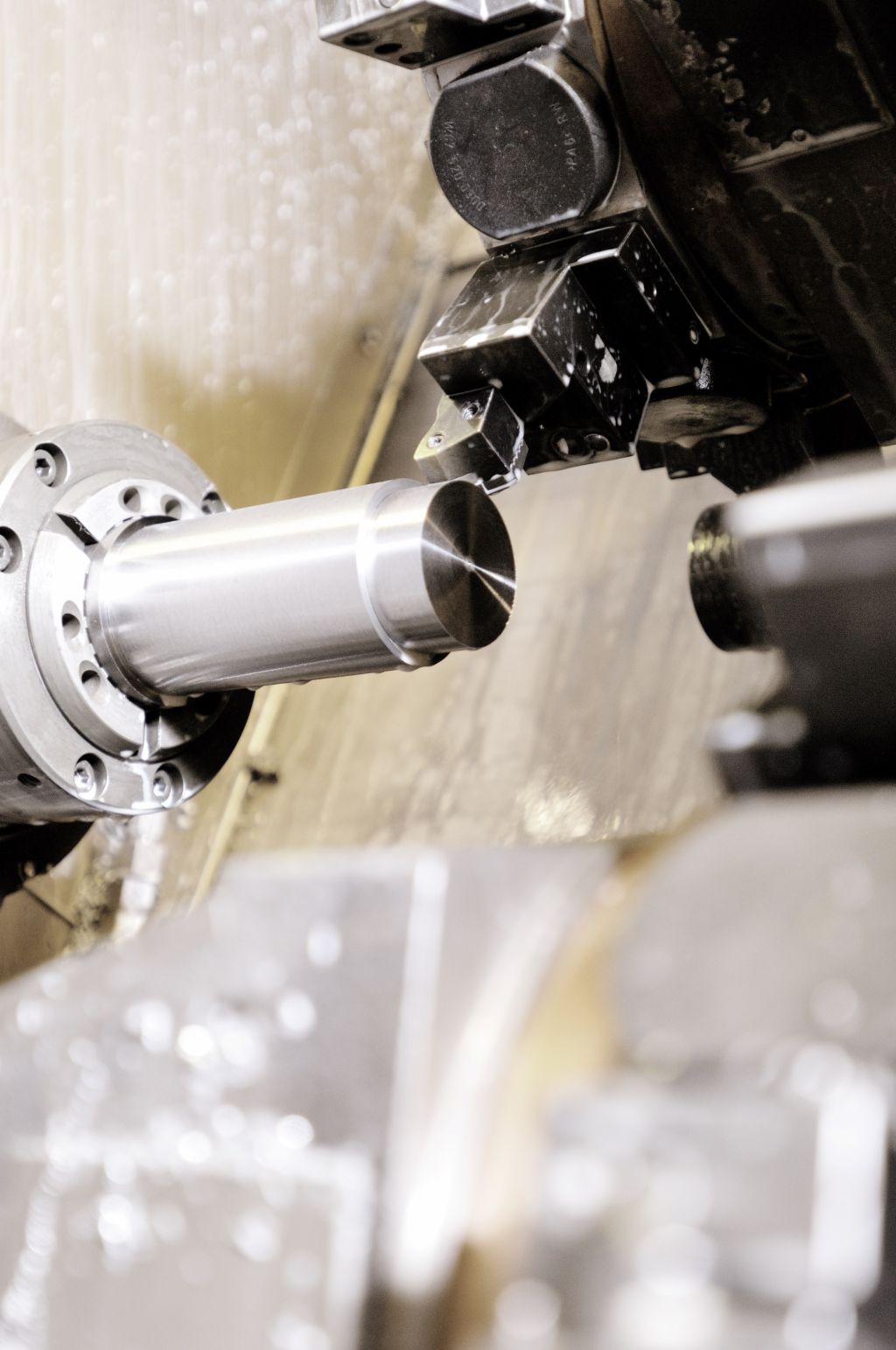

Amid cost pressure and supply security, the machining industry is currently particularly focused on the availability of tungsten and carbide. Rising tool prices and vulnerable supply chains are increasing the pressure on companies. At the same time, efficient processes, alternative tool concepts, and stable procurement strategies are becoming more prominent. The spring conference of the Association of the German Turned Parts Industry made it clear how intensively the industry is addressing these developments.

What begins on the international raw material markets is now directly affecting the calculations of turned parts manufacturers. Tungsten is a central component of modern carbide tools and is indispensable for machining processes. High cutting speeds, economical tool life, and process reliability are hardly achievable in numerous applications without carbide.

The members of the Association of the German Turned Parts Industry are also closely monitoring the price and availability developments. A consistent picture emerges: It is no longer just about rising raw material prices. The strong concentration of tungsten mining and processing in China makes European industries vulnerable. Political tensions, trade conflicts, or export restrictions have a direct impact on supply chains and markets.

"The massive price increases of the past months can unfortunately no longer be compensated," says Markus Horn from the tool manufacturer Horn. "Trust in the supply chain has suffered significantly." As a result, an issue that was previously operational in procurement is increasingly becoming a strategic challenge for the entire value chain.

Price pressure and limited scope

The effects are clearly noticeable in manufacturing. Tool and carbide prices are rising significantly in some cases, competitive pressure is high, and many customers expect stable prices.

"While on one hand we cannot resist these increases, it is hardly, if at all, possible to pass them on to our customers," describes Julius Klinke from the turned parts manufacturer Julius Klinke the situation. Many companies feel compelled to bear a portion of the additional costs themselves.

Other companies are also feeling the pressure. The Saxon precision turned parts manufacturer SUSA Sauer reports a significant effort to continuously assess price developments and incorporate them into calculations. Constant cost adjustments and short offer deadlines complicate project planning and tie up additional capacities. Maier, also a specialist in precision technology, reports similar challenges. In particular, fluctuating raw material costs make reliable pricing difficult, while the demands for reaction speed are increasing. A similar situation is evident at the carbide special tool manufacturer Prinzbach. The company points to the high volatility in the raw material markets. Orders need to be recalculated much more frequently, while long-term price commitments and reliable planning are becoming increasingly difficult.

In addition to costs, availability is becoming a greater focus. The supply of carbide tools is currently still largely stable, but delivery times are extending for certain products. This is confirmed by Heinrichs Drehteile and Kößler. The two manufacturers of precision turned parts report delivery times of more than four weeks for standard tools and are experiencing initial bottlenecks. Many companies expect that the situation could worsen as the year progresses. Accordingly, they need to plan ahead for their

Plan procurement processes.

There is broad consensus regarding the assessment of international dependencies: The European machining industry is heavily reliant on Asian, particularly Chinese, suppliers. About 80 percent of the world's tungsten is sourced from China. Accordingly, there is a growing desire for diversified supply chains, stronger European recycling capacities, and an independent raw material strategy.

Technical answers instead of renunciation

The companies are not responding by waiting. An alternative to carbide is hardly being discussed at the moment.

The advantages of the material in terms of tool life, productivity, and process reliability are too significant for that. Instead, companies are focusing on a more efficient use:

optimized cutting geometries, modern coatings, multi-edged tools, as well as consistent re-sharpening and refurbishment. Alternative material concepts such as cermet are also gaining importance in certain applications.

"The current situation with tungsten and hard metal is very tense for us," explains Stefan W. Schauerte. "Due to the strong and short-term price developments, tool costs are hardly calculable at the moment." Schauerte is a manufacturer of precision turned parts with its own tool grinding shop and is focusing on sharpening tools more intensively and with greater material awareness, reworking them when necessary, and using crown tools whenever possible, which require significantly less raw material than complete solid carbide solutions. KOWE operates similarly with a focus on resource efficiency. The company utilizes modern coatings, reconditioned tools, and interchangeable head systems in its turned part production.

A glance into the future

Tungsten and hard metal will remain indispensable for machining for the foreseeable future. At the same time, rising costs, geopolitical risks, and a strong concentration of supply chains are increasing pressure on the industry. Therefore, the answer is not abstinence, but efficiency: longer tool life, smarter tool concepts, consistent recycling, and the most economical use of a material that remains irreplaceable for many applications.

Association Managing Director Werner Liebmann sees this as a central path for the coming years: "Companies continue to face significant pressure, but they are responding very quickly and flexibly to the new conditions. This innovative strength will be crucial to ensure the long-term competitiveness of the machining industry."

Contact: